4 Crude Steps to Not Being Broke

It repeatedly blows me away how many people I know, from all walks of life, know absolutely nothing about their money. Most of them would cite making more money or (insert dream here that costs more money) as one of their primary goals if you asked, yet their actions are often leading them in the complete opposite direction. I'm certainly no expert, but here are some of the basics that I've picked which seem in desperate need of sharing. Please feel free to add any relevant additional information in the comments.

Also I should mention that reddit.com/r/personalfinance is a great resource with tons of quality information. You can click the link above for a more detail than I'll ever write. For those of you as lazy as I am, below are the Spark Notes(ish).

0. Stop Buying Shit You Can't Afford and Don't Really Want

Just because the person next to you bought a bedazzled Pokemon iPhone case doesn't mean you need to buy a brand-new convertible BMW. If you really want something, save up for it. The process of delaying gratification will help you weed out the crap that you don't actually want and will also make it more satisfying when you do get it.

*I personally believe (and some research supports) money is far better spent on experiences (travel, concerts, cooking lessons, etc.) than on things (clothes, electronics, cars, etc.). Learn more here.

1. Create a Budget

For those that can do basic math and would like to improve their chances of not ending up bitching amount money for the rest of their lives, take these simple steps:

2. Build an Emergency Fund

This is a duh. You should have enough in cash to cover 3-6 months of expenses. If you're paying down credit card debt, then a smaller amount (minimum 1 month of expenses) is ok while you pay it off. Click here for specifics on determining the size of your emergency fund. Setup a recurring transfer to your savings account that matches when you get paid. If you don't have a savings account, set that up. Do it NOW.

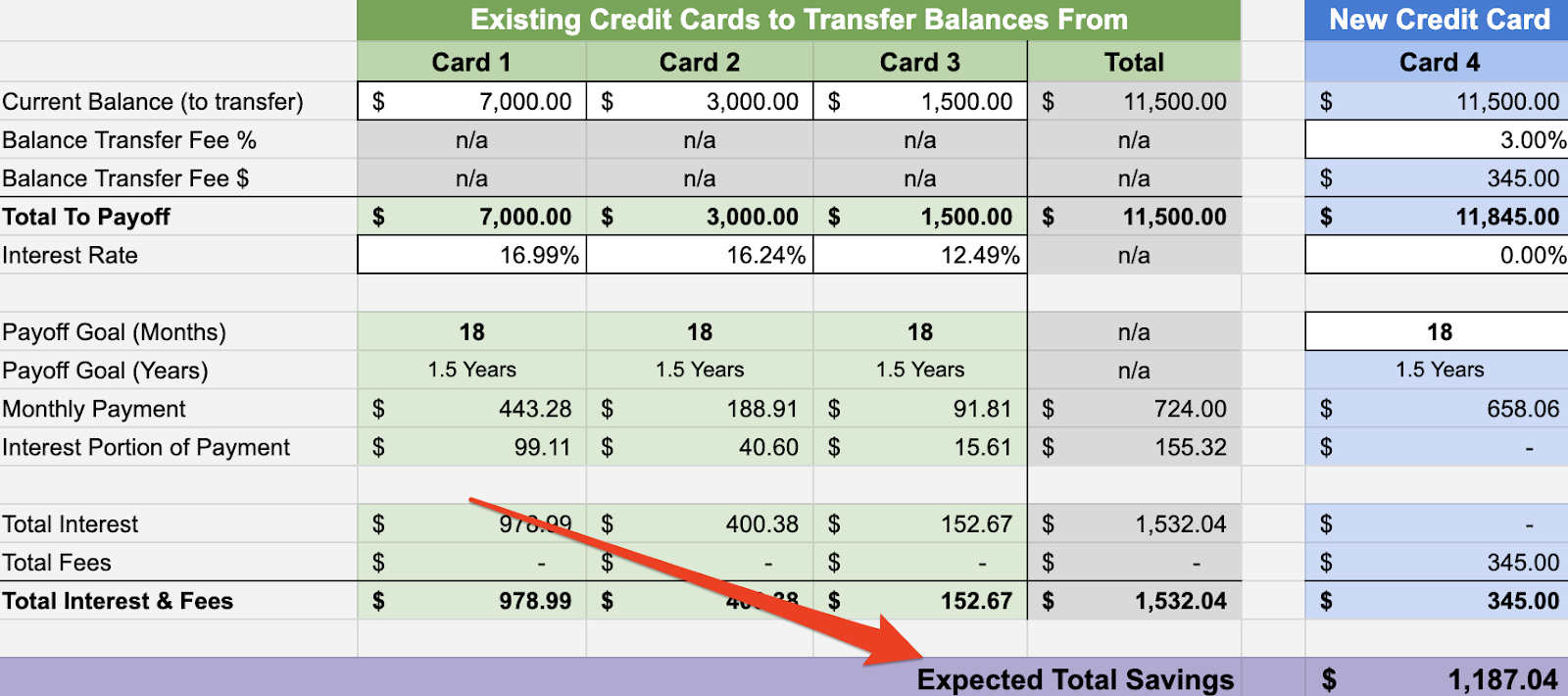

3. Understand Credit Cards and Pay Them Off

It's called compound interest, and it's designed to fuck you. The credit card companies know this well, which is why they're always offering a million incentives to sign up for a new card. While leveraging credit appropriately can be important for obtaining financing later in life for large purchases such as a home, the overall consensus is that you should stay away from credit cards as much as possible.

To keep this simple, here are what I find to be the most important Do's and Dont's:

4. Max Out Employer Matching of Retirement Funds

If your employer offers one of these plans and you do not max it out (contribute the full amount that gets matched) you are literally leaving free money on the table.

These are the steps that you should take now. Not tomorrow, or next week, but now. If you have any questions please feel free to ask.

Also I should mention that reddit.com/r/personalfinance is a great resource with tons of quality information. You can click the link above for a more detail than I'll ever write. For those of you as lazy as I am, below are the Spark Notes(ish).

0. Stop Buying Shit You Can't Afford and Don't Really Want

Just because the person next to you bought a bedazzled Pokemon iPhone case doesn't mean you need to buy a brand-new convertible BMW. If you really want something, save up for it. The process of delaying gratification will help you weed out the crap that you don't actually want and will also make it more satisfying when you do get it.

*I personally believe (and some research supports) money is far better spent on experiences (travel, concerts, cooking lessons, etc.) than on things (clothes, electronics, cars, etc.). Learn more here.

|

| Seeing the World > Your Next Stupid Purchase |

For those that can do basic math and would like to improve their chances of not ending up bitching amount money for the rest of their lives, take these simple steps:

- Write down all of your fixed monthly expenses (mortgage/rent, utilities, car payment, insurance, etc.)

- Write down all of your estimated variable expenses (food & dining, gas, entertainment, shopping, etc.)

*Using a tool such as mint.com can be very useful in analyzing your spending habits - Total these expenses and subtract them from your monthly income - if you aren't left with a positive number, re-read Step 0 and then adjust your variable expenses.

2. Build an Emergency Fund

This is a duh. You should have enough in cash to cover 3-6 months of expenses. If you're paying down credit card debt, then a smaller amount (minimum 1 month of expenses) is ok while you pay it off. Click here for specifics on determining the size of your emergency fund. Setup a recurring transfer to your savings account that matches when you get paid. If you don't have a savings account, set that up. Do it NOW.

3. Understand Credit Cards and Pay Them Off

It's called compound interest, and it's designed to fuck you. The credit card companies know this well, which is why they're always offering a million incentives to sign up for a new card. While leveraging credit appropriately can be important for obtaining financing later in life for large purchases such as a home, the overall consensus is that you should stay away from credit cards as much as possible.

To keep this simple, here are what I find to be the most important Do's and Dont's:

- Don't let your credit card balance exceed 30% of your credit limit - important for your credit score

- Don't have more than two credit cards - one is plenty

- Don't open credit cards through a specific store - their interest rates are typically higher and perks significantly less

- Do borrow from your savings (non-emergency fund savings) for large expenses and simply pay yourself back at 0% interest instead of using a credit card if at all possible

- Do pay off 95-100% of your statement balance every month - setting up an automatic payment for the full balance each month is ideal

- Do make your payment in the same month the statement closes - if you wait until the payment is due you are simply procrastinating and setting yourself up for cash flow problems if you experience a decrease in income

- Do use a card with strong travel rewards for all reimbursable work travel - I recommend the Chase Sapphire Preferred or Barclaycard Arrival + as they both have good rewards programs and no foreign transaction fees

4. Max Out Employer Matching of Retirement Funds

If your employer offers one of these plans and you do not max it out (contribute the full amount that gets matched) you are literally leaving free money on the table.

These are the steps that you should take now. Not tomorrow, or next week, but now. If you have any questions please feel free to ask.